Sustainability (and the English language!) can be confusing. Terminology abounds. If you’re looking to have your greenhouse gas (GHG) emissions independently evaluated you will quickly find out there are many different words used: verification, validation, assurance, certification, audit. How do they differ? What’s right for your organisation? Where do you start?

Here’s some advice on how these terms intersect and differ and recommendations to help you choose what’s right for your organisation.

What these terms have in common

All terms used recognise two things:

Evaluating your GHG emissions is a good thing to do. Evaluation helps you check your data, keeps you accountable for meeting your targets, and equips you to set new targets. It ensures you comply with legal reporting standards and can talk about your progress publicly without risking ‘greenwash’. The process of evaluation can be valuable too. You’re likely to learn something about your business (and your emissions) that you didn’t know before.

Independence matters. A third party takes an arm’s-length view of your emissions. Independence brings with it peace of mind – for your organisation (including your board members or trustees) and your stakeholders (including your investors, regulators, customers and members).

Where these terms diverge

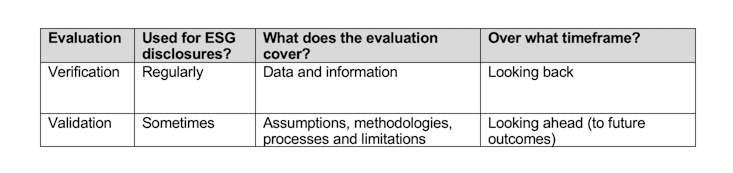

Verification and validation are processes. Of the two, verification is the more exacting and the more common.

Here’s your bible: ISO 14064-3:2019. It’s best practice guidance, it’s used globally, and it covers both verification and validation. ISO 14064 offers these definitions (I have added the emphasis):

Verification: a process for evaluating a statement of historical data and information to determine if the statement is materially correct and conforms to criteria

Validation: a process for evaluating the reasonableness of the assumptions, limitations and methods that support a statement about the outcome of future activities

The outcome of a verification can be limited or reasonable assurance. More on this below.

Assurance (reasonable and limited) is an outcome, generally from verification. That is, it focuses on data and information. Here are the ISO 14064-3 definitions. Again, the emphasis is ours.

Reasonable assurance: a level of assurance where the nature and extent of the verification activities have been designed to provide a high but not absolute level of assurance on historical data and information.

Limited assurance: a level of assurance where the nature and extent of the verification activities have been designed to provide a reduced level of assurance on historical data and information.

Assurance can be a process too. To make things a tad more complicated, GHG emissions can be assured (a process) as well as verified. In Australia, reporting is mandatory for registered corporations under the National Greenhouse and Reporting (NGER) Act. The Regulator may require reasonable or limited assurance if they reasonably suspect a company, relevant person or entity of contravening the Act.

In New Zealand, the new standard from the External Reporting Board for TCFD (Task Force for Climate-related Disclosures) reporting, which includes GHG emissions, will require limited assurance. This may increase to reasonable assurance over time. Similarly, the New Zealand government requires its departments to report and assure their GHG inventories from the 2022/2023 financial year. You’ll find more information here at page 22: A Guide to measuring and reporting GHG emissions.

Audit has several meanings. In many ways, the smallest word is the hardest to define. The term ‘audit’ tends to be used in a general way as in: ‘We’ve audited our carbon footprint.’ It can refer to the initial inventory of an organisation’s carbon footprint or the independent evaluation that follows (whether a verification, a validation or an assurance).

The New Zealand External Review Board (XRB) gives ‘audit’ a specific meaning (our emphasis): An audit is a reasonable assurance engagement over historical financial information.

The XRB also introduces a new term (‘review’): A review is a limited assurance engagement over historical financial information that is less thorough and detailed than an audit.

Audits may also be undertaken as part of compliance monitoring and management.

Certifications can take many forms. While many are associated with offsets, some relate to carbon too. For example, in Australia, the reputable Climate Active Certification proves that a business or organisation has achieved net zero emissions. In Aotearoa New Zealand, Ekos and Toitū offer well-respected carbon certifications.

Certification schemes commonly link to the ISO standards for GHG reporting but there may be other requirements for certification too. These could include producing and rolling out an emissions reduction plan and reporting performance annually.

What we recommend:

Have your emissions reviewed annually by an experienced third party.

Choose verification over validation – it’s a more exacting process.

Keep an eye on changing reporting standards. They increasingly require assurance.

If you’ve had your emissions verified, take the next step and set a Science-based Target (SBT). You’re already measuring and reviewing. Now drive your emissions down with an ambitious target.

Tread carefully with certifications. If you go down this route, choose a reputable one such as the ones listed above. Sustainability is about impact, not branding!

Note: thinkstep-anz is not an accredited GHG verification body. Their expertise are in helping organisations measure GHG emissions and set a plan to reduce them, including Scope 3 (value chain) emissions.

This article was originally posted on the thinkstep-anz blog at https://www.thinkstep-anz.com/resrc/blogs/verify-validate-assure/.